Bilt has garnered significant attention for its suite of credit cards, particularly following a rocky initial rollout that may have caused some consumers to undervalue the broader ecosystem. While the Bilt Palladium Card is a powerful tool—offering an effective 3.3x return on spending when combined with housing payments and transfer bonuses—it represents only a fraction of the company’s strategy.

The critical insight for consumers is this: You do not need a Bilt credit card to access their highly valued transferable points. In fact, the vast majority of Bilt’s user base operates without one.

The Non-Card Majority

Bilt reports over 5 million members, yet only 15% hold a Bilt co-branded credit card. This means approximately 750,000 users have cards, while over 4 million members are earning points through the platform without ever applying for a Bilt-issued product.

This demographic shift highlights a fundamental change in how Bilt operates. Rather than being solely a credit card issuer, Bilt functions primarily as a property management software provider, payment processor, and loyalty platform. The credit cards are merely one entry point into a much larger financial ecosystem.

How to Earn Points Without a Bilt Card

For the 4 million users without a Bilt card, the platform offers robust ways to accumulate points by linking existing credit cards. Users can connect their current Visa, Mastercard, Amex, or other cards to their Bilt wallet to earn rewards through specific partner categories.

Key earning opportunities include:

- Dining: Points via Bilt’s bespoke partnerships and Rewards Network restaurants.

- Transportation: Lyft rides and Metropolis parking.

- Fitness: Bookings at major chains like SoulCycle, Barry’s, CorePower Yoga, and YogaSix.

- Shopping: Purchases through the Rakuten shopping portal, Walgreens, GoPuff, and BLADE.

- Travel: Flights booked through the Bilt travel portal earn 1 point per dollar.

By linking existing cards, users can access these rewards without changing their banking habits or incurring new annual fees. Currently, 89% of linked cards in Bilt wallets are from other issuers, with Visa (56%) and Mastercard (32%) dominating the landscape.

The Value of Bilt Points

The reason so many users engage with the platform—even without a card—is the quality of the points themselves. Bilt points are highly flexible, offering transfers to a wide array of airline and hotel partners. This flexibility allows users to maximize value, especially when transfer bonuses are available.

Airline Partners:

* Star Alliance: Air Canada Aeroplan, Turkish Miles & Smiles, United MileagePlus, Avianca LifeMiles, TAP Air Portugal.

* oneworld: Cathay Pacific Asia Miles, Alaska Airlines Mileage Plan, Iberia Plus, British Airways Executive Club, Japan Airlines, Qatar Airways.

* SkyTeam: Air France-KLM Flying Blue, Virgin Atlantic Flying Club.

* Non-Alliance: Emirates Skywards, Southwest Airlines, Aer Lingus AerClub.

Hotel Partners:

* World of Hyatt, IHG One Rewards, Marriott Bonvoy, Hilton Honors, Accor ALL, and Wyndham Rewards.

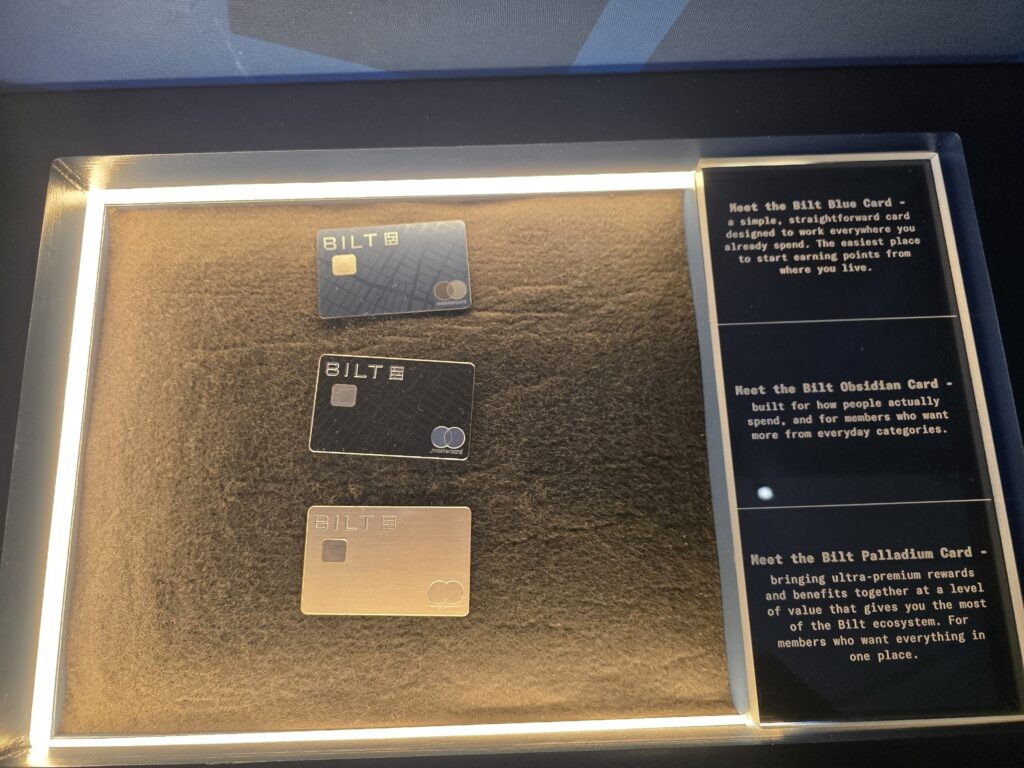

For users who do choose to get a Bilt card, the value proposition is strong. The Bilt Blue Card ($0 annual fee) can yield up to 2.3 transferable points per dollar when combined with housing payments. The Bilt Obsidian Card ($95 annual fee) offers 3x points on groceries or dining and 2x on travel, potentially reaching 4.3 points per dollar on key categories. However, these cards are optional enhancements, not requirements, for a rewarding experience.

Why This Model Matters

Bilt’s success is not just about credit cards; it is about distribution. The company has solved a major challenge in fintech: reaching high-value customers in a “sticky” environment. By integrating into the housing payment process—processing rent and mortgage payments for 1 in 4 U.S. rental buildings—Bilt has embedded itself into the most significant financial transaction many people make.

The company expects to process over $100 billion in housing payments in 2026, capturing roughly 5% of the market. This infrastructure allows Bilt to acquire customers uniquely, offering them rewards and benefits tied to their homes and neighborhoods.

Bilt’s recent funding round, which valued the company at over $10 billion, reflects investor confidence in this novel model. They have monetized housing relationships by rewarding customers richly while maintaining a low-friction entry point for those who prefer not to carry a new credit card.

Conclusion

Bilt is more than a credit card company; it is a comprehensive loyalty platform anchored in housing payments. While its cards offer high returns for those who qualify, the core value lies in the ability for millions of users to earn transferable points on everyday spending through existing cards. This approach makes Bilt one of the most ambitious and accessible loyalty programs since the dawn of modern airline miles.

{kind=link}